Every Little Thing You Needed To Know About Residence Mortgages

Article written by-McMahan SimpsonA lot of people are so willing to jump at the first home mortgage they find that they end up getting burned by an unstable, variable loan. This is obviously something you want to avoid and thus you need a good understanding of how the industry works. Below, you will read some great tips pertaining to home mortgages and how you can get a good loan.

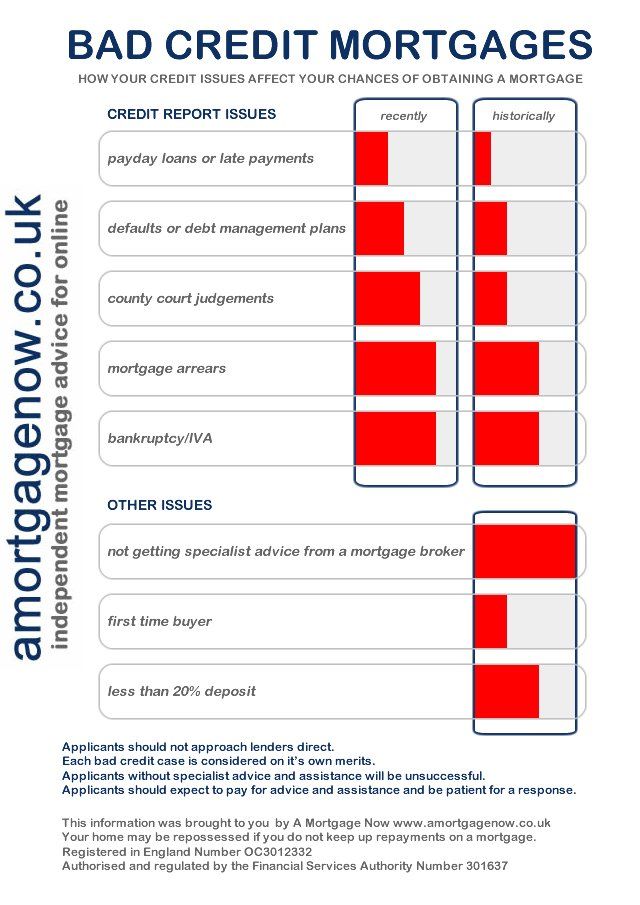

Predatory lenders are still in the marketplace. These lenders usually prey on home buyers with less than perfect credit. They offer low or no down payments; however, the interest rates are extremely high. Additionally, these lenders often refuse to work with the homeowner should problems arise in the future.

Check your credit report before applying for a mortgage. With today's identity theft problems, there is a slight chance that your identity may have been compromised. By pulling a credit report, you can ensure that all of the information is correct. If you notice items on the credit report that are incorrect, seek assistance from a credit bureau.

When considering the cost of your mortgage, also think about property taxes and homeowners insurance costs. Sometimes lenders will factor property taxes and insurance payments into your loan calculations but often they do not. You don't want to be surprised when the tax office sends a bill and you learn the cost of required insurance.

Know your credit score before beginning to shop for a home mortgage. If your credit score is low, it can negatively affect the interest rate offered. By understanding your credit score, you can help ensure that you get a fair interest rate. Look At This require a credit score of at least 680 for approval.

Understand the difference between a mortgage broker and a mortgage lender. There is an important distinction that you need to be aware of so you can make the best choice for your situation. A mortgage broker is a middle man, who helps you shop for loans from several different lenders. A mortgage lender is the direct source for a loan.

Friends can be a very good source of information when you need a mortgage. They may be able to provide you with some advice that you need to look out for. Some may share negative stories that can show you what not to do. When you talk to more people, you're going to learn more.

You likely know you should compare at least three lenders in shopping around. Don't hide this fact from each lender when doing your shopping around. They know you're shopping around. Be forthright in other offers to sweeten the deals any individual lenders give you. Play them against each other to see who really wants your business.

If your appraisal isn't enough, try again. If the one your lender receives is not enough to back your mortgage loan, and you think they're mistaken, you can try another lender. You cannot order another appraisal or pick the appraiser the lender uses, however, you may dispute the first one or go to a different lender. While the appraisal value of the home shouldn't vary drastically too much between different appraisers, it can. If you think the first appraiser is incorrect, try another lender with, hopefully, a better appraiser.

Before you apply for a mortgage, know what you can realistically afford in terms of monthly payments. Don't assume any future rises in income; instead focus on what you can afford now. Also factor in homeowner's insurance and any neighborhood association fees that might be applicable to your budget.

Save up enough so you can make a substantial down payment on your new home. Although it may sound strange to pay more than the minimum required amount for the down payment, it is a financially responsible decision. You are paying a lot more than the asking price for the home with a mortgage, so any amount that you pay ahead of time reduces the total cost.

When trying to figure out how much of a mortgage payment you can afford every month, do not neglect to factor in all the other costs of owning a home. There will be homeowner's insurance to consider, as well as neighborhood association fees. If you have previously rented, you might also be new to covering landscaping and yard care, as well as maintenance costs.

You must be demonstrably responsible to get a home mortgage. This means you have to have a good job that pays for your lifestyle with money to spare. Not only that, you must have been on the job for a couple of years or more, and you must be a good employee. The home mortgage company is entering into a long term relationship with you, and they want to know that you are ready to commit seriously!

Extra payments will be applied directly to your loan amount and save you money on interest. This will help you get the loan paid off quicker. For instance, paying just an extra $100 every month can lower your term by ten years.

Understand what happens if you stop paying your home mortgage. It's important to get what the ramifications are so that you really know the seriousness of such a big loan as a home mortgage. Not paying can lead to a lower credit score and potentially losing your home! It's a big deal.

Make sure that you compare mortgage rates from several companies before you settle on one. Even if the difference seems to be minimal, this can add up over the years. One point higher can mean thousands of extra you will have to shell out over the course of the loan.

If you don't have any credit history, you might have to find alternative sources for a loan. Keep your receipts for a year. Demonstrating timely payments for things like utilities and rent is useful for those without extensive credit histories.

Whenever you struggle to make mortgage payments, speak to your lender immediately. They can help you to reduce your interest rates by extending your mortgage, or can give you tips on your personal situation and how you can change your finances to help you keep paying for your home every month.

During the process of obtaining a mortgage loan, submit any requested documents to your mortgage broker or lender as soon as possible. Taking your time to respond to your lender can delay the date of the closing. Delaying https://www.pymnts.com/credit-unions/2021/truliant-federal-credit-union-on-personalizing-digital-first-business-banking/ closing date can put you at risk of losing the rate you have locked-in.

You must take the time to learn how to obtain the home loan that is right for you before applying for one. You want to find a home you can afford at the best rate possible for your situation. You don't want a home you can't afford. In the end, what you want is a home you can enjoy for years and a lender who is understanding and fair.